Mumbai, May 21: There is a particular kind of corporate acquisition that looks, on the surface, like a routine asset purchase but reveals itself on closer reading to be something considerably more calculated.

Adani Ports and Special Economic Zone Ltd’s decision to acquire Kanpur Fertilizers and Cement Limited (KFCL) for roughly ₹1,500 crore is exactly that kind of deal. The numbers, taken alone, are unspectacular. A mid-sized fertilizer and cement maker in Uttar Pradesh, carrying the weight of past debt troubles, changing hands for a sum that barely registers in the Adani Group’s broader capital story.

But trace how this fits into Adani Ports’ existing port network, rail links, agri-warehousing assets, and food distribution arm and the picture sharpens considerably. Adani Ports is not simply buying a fertilizer company. It is buying a node in a supply chain it has been quietly assembling, piece by piece, for years.

Adani Ports and the KFCL Deal: What Is Actually Happening

Kanpur Fertilizers and Cement Limited is not a name that regularly features in investor pitch decks. The company has been around long enough to weather multiple agricultural policy cycles, several natural gas price shocks, and at least one serious financial crisis that pushed it through debt restructuring in recent years. Its core product is urea the single most consumed fertilizer in India. It also runs a cement operation serving construction demand across UP and neighbouring states.

What KFCL has built over the decades, however, is harder to replicate than its balance sheet suggests. Its distribution network gives it genuine last-mile reach into rural agricultural markets across the Hindi heartland the kind of on-ground presence that no amount of fresh capital can quickly recreate.

India consumes somewhere between 33 and 35 million metric tonnes of fertilizers every year, per figures from the Department of Fertilizers. Domestic production, despite years of government incentives, still falls short of that demand. The gap gets plugged by imports which means price volatility, currency exposure, and supply chain fragility that governments hate and farmers ultimately absorb.

A domestic manufacturer like KFCL, imperfect as it may be financially, sits on an asset base that is structurally useful precisely because it is local, distributed, and already embedded in the agricultural input supply chain at the ground level.

Why Adani Ports Is Moving Beyond Pure Port Operations

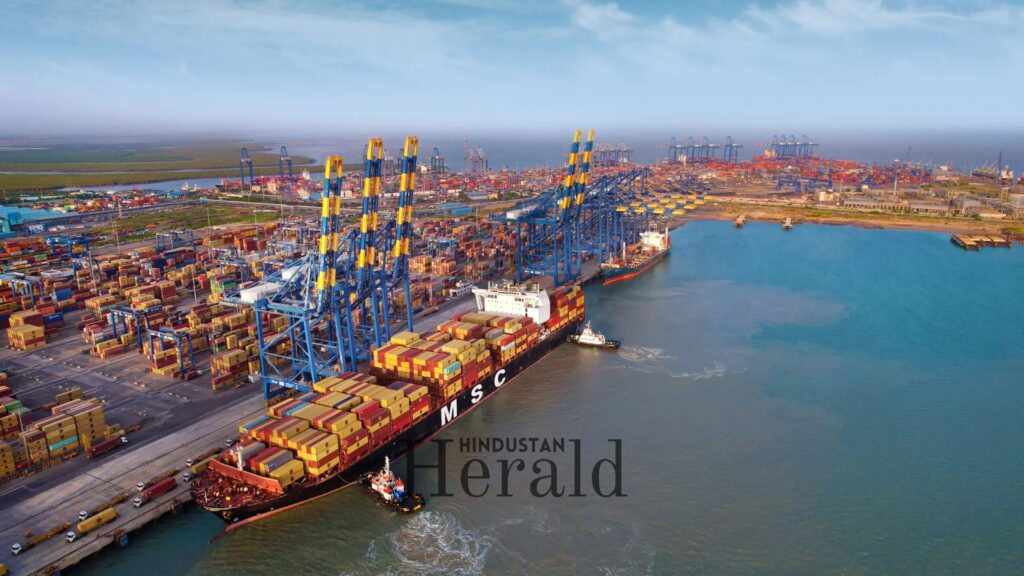

Here is the tension at the heart of Adani Ports’ business model that this acquisition is designed, at least partially, to resolve. Adani Ports runs across 13 major ports, operates one of India’s largest inland logistics networks, and crossed 400 million metric tonnes in cargo volumes in fiscal year 2024. By every conventional measure, it is performing exceptionally well. And yet, the ceiling on pure port-based growth is more visible than it used to be.

Port tariffs are regulated. The government’s Sagarmala Programme has been pouring capital into state-owned ports, which are getting faster and more competitive every passing year. Internationally, Adani Ports has expanded the Haifa Port acquisition in Israel in 2022 being the most prominent example but there are natural limits to growing a logistics business by simply adding more ports to a network.

The smarter path, the one Adani Ports leadership appears to have firmly settled on, is to own what flows through the network rather than just charge for its passage. If your ports handle fertilizer imports, why not manufacture fertilizer domestically and route it through those same berths? If your rail links connect UP’s industrial belt to coastal export hubs, why not own the factory at one end and the terminal at the other?

This is vertical integration but more deliberate than the textbook variety. It is a systematic effort to make Adani Ports’ logistics infrastructure indispensable by ensuring the cargo it handles has no obvious reason to go elsewhere.

Adani Ports and the Subsidy Safety Net Nobody Talks About

One detail of this deal that deserves far more attention is the financial character of India’s fertilizer business and what the government’s subsidy architecture means for Adani Ports as an acquirer.

India’s fertilizer subsidy bill for 2024-25 was budgeted at approximately ₹1.64 lakh crore. The government essentially guarantees domestic urea manufacturers a controlled price that covers production costs, because the alternative letting prices float freely would devastate farm economics and carry enormous political consequences.

In practice, this means the largest effective customer for any Indian urea maker is the Union government itself which also happens to be the most reliable payer in the economy. For Adani Ports, trying to de-risk a manufacturing investment, that is an unusually stable starting position to acquire.

The risks are not zero. Natural gas prices which determine a large chunk of urea production costs can be volatile, as they were through 2022 and 2023. Subsidy disbursements have historically arrived with delays that squeeze working capital. And the PM Pranam scheme, which nudges states toward reducing chemical fertilizer usage, along with IFFCO’s nano urea push, introduces some longer-term demand-side uncertainty. None of that is an existential threat in the near term. But it is worth watching closely as the decade unfolds.

What Adani Ports Gets From KFCL’s Cement Business

KFCL’s cement business is, by most readings, the less strategically exciting piece of this deal for Adani Ports. That said, it is not without value.

Uttar Pradesh is running one of the most active construction programmes in its modern history. The Ganga Expressway, the Bundelkhand Expressway, the PM Awas Yojana housing rollout, and Smart Cities Mission projects across Lucknow, Kanpur, Varanasi, and Agra are collectively pushing cement demand well above national growth averages. According to data cited by Business Standard from the Cement Manufacturers Association of India, UP’s cement consumption has been consistently growing at a clip that outpaces the all-India average by several percentage points.

Still, it would be a stretch to frame this as a cement play for Adani Ports. The group already controls over 70 million tonnes per annum of cement capacity through ACC and Ambuja Cements, making it India’s second-largest cement producer. KFCL’s cement volumes are modest in that context. The more likely outcome is that the cement operations get absorbed into the group’s regional supply network useful, contributing, but not the strategic centrepiece.

Adani Ports and the Real Price of This Acquisition

The headline figure of ₹1,500 crore deserves some honest unpacking. Adani Ports is paying what market observers broadly describe as a post-restructuring, compressed-multiple price the kind of valuation that reflects an asset’s recent financial difficulties more than its underlying strategic usefulness.

Fertilizer manufacturing businesses in India have long traded at lower multiples than comparable sectors for two well-understood reasons. First, subsidy-linked revenue is harder to model cleanly for equity investors. Second, feedstock exposure to gas prices means profitability can swing sharply as the entire industry experienced during the global energy disruptions of 2022 and 2023.

For a strategic buyer like Adani Ports, with its existing balance sheet depth and gas logistics infrastructure already in place, both risks are considerably more manageable than they would be for a standalone operator. That gap between perceived risk and actual manageability, for a buyer of Adani Ports’ scale, is precisely where the value sits.

One important caveat: whether the deal includes assumption of KFCL’s legacy debt has not been fully disclosed in regulatory filings at the time of this report. If it does, the total enterprise value will be meaningfully higher than the equity consideration alone. Market participants are waiting on full deal structure disclosure under SEBI listing obligations before reaching a final verdict.

The Larger Supply Chain Puzzle Adani Ports Is Assembling

Step back from the KFCL transaction and what comes into view is Adani Ports methodically closing the gaps in an agricultural value chain that, if fully assembled, would have very few parallels in the Indian private sector.

Adani Wilmar handles edible oils and packaged food, with a rural retail reach stretching into India’s deepest agricultural markets. Adani Agri Logistics operates cold chain and warehousing infrastructure, storing grain and perishables for both government procurement programmes and private clients.

Adani Ports’ own port and rail network moves agricultural inputs and processed food exports at considerable scale. And now KFCL adds fertilizer manufacturing and ground-level input distribution the upstream end of the chain to that picture.

The only other Indian conglomerates that have attempted anything approaching this level of agri-value-chain integration are ITC, through its e-Choupal network, and Reliance, through JioMart and its rural retail expansion. Neither has combined port infrastructure, fertilizer production, cold chain logistics, and food processing under one umbrella with the internal freight logic that makes every piece more valuable because of the others. That is the system Adani Ports is building toward one carefully chosen acquisition at a time.

Adani Ports: Regulatory Outlook and What Comes Next

The deal’s regulatory pathway looks reasonably clean. The Competition Commission of India is unlikely to raise serious concerns. KFCL’s share of national fertilizer manufacturing capacity is not large enough to trigger horizontal concentration issues, and the combination of a port operator with a fertilizer manufacturer does not present the kind of vertical foreclosure argument that typically draws prolonged regulatory scrutiny.

No foreign investment clearances are required. Both entities are domestically incorporated, and the transaction is expected to move through standard CCI review within three to six months of announcement.

For Adani Ports minority shareholders, the key question remains capital efficiency. The company has maintained a return on equity consistently above 14 percent over the last three financial years, per its NSE filings. Whether KFCL eventually contributes to or dilutes that figure depends almost entirely on how quickly the fertilizer plant can be modernised and how effectively Adani Ports monetises the supply chain integration it is banking on.

Adani Ports and the Market Verdict That Will Matter Most

Adani Ports shares have recovered substantially over the past two years, clawing back ground lost after the Hindenburg Research report rattled the group in early 2023. Institutional confidence has returned gradually, but tangibly.

How the market responds to the KFCL acquisition will signal whether that confidence now extends to the group’s agricultural diversification thesis. A sustained positive reaction would suggest investors see the value chain logic as commercially sound. A muted or negative response would raise questions about whether shareholders want Adani Ports deploying capital outside its core port and logistics identity.

For the farmers across UP who buy KFCL’s urea at the government-mandated subsidised price, very little about this transaction will feel significant in the short term. The bags of fertilizer will still arrive at the same mandis, priced the same way, through much the same distribution chain they have always relied on.

What will have changed is who owns the factory and what they plan to do with the road between that factory and the sea. That road, as it happens, runs straight through the heart of everything Adani Ports has been building for the last two decades.

Stay ahead with Hindustan Herald — bringing you trusted news, sharp analysis, and stories that matter across Politics, Business, Technology, Sports, Entertainment, Lifestyle, and more.

Connect with us on Facebook, Instagram, X (Twitter), LinkedIn, YouTube, and join our Telegram community @hindustanherald for real-time updates.

Tracking world politics, global markets, trade movements, policy decisions, and the changing balance of economic power.

- Shelesh Joshi

- Shelesh Joshi

- Shelesh Joshi

- Shelesh Joshi

Former financial consultant turned journalist, reporting on markets, industry trends, and economic policy.

- Kavita Iyer

- Kavita Iyer

- Kavita Iyer

- Kavita Iyer