Mumbai, May 21: The Hormuz blockade is no longer a distant geopolitical headline. It is sitting inside India’s economy right now, squeezing crude supply, battering the rupee, and forcing the Reserve Bank into decisions it does not want to make.

President Donald Trump told reporters this week that talks with Iran were in their “final stages,” and warned Tehran of “some very nasty things” if no deal materialised. He sounded, depending on your read of the man, either like someone genuinely close to a historic agreement or like someone buying time before the next escalation. Nobody really knows which one it is. And for India, that uncertainty is not abstract. It is showing up in OMC balance sheets, in central bank press conferences, and eventually, in the price of everything.

Hormuz Blockade: How A Threat Nobody Took Seriously Became Reality

To understand where things stand today, you have to go back about a year. When Trump returned to the White House in early 2025, he wanted an Iran deal. Not the Obama-era JCPOA he had torn up in his first term, but something bigger, something he could brand as his own. Talks started through Oman. There was cautious progress. Diplomats briefed journalists in careful, hedged language about momentum and goodwill.

Then, in June 2025, the whole thing fell apart. What followed was the Twelve-Day War, a short, sharp military exchange that ended with US and Israeli strikes on Iran’s nuclear facilities. The strikes were surgical in intent. The aftermath was anything but.

Iran came out of that conflict damaged, furious, and still standing. Its enrichment programme had taken a hit. Its international standing had taken a hit. But its missiles were intact, its allied networks across the region were intact, and most importantly, its grip over the Hormuz blockade trigger was completely intact.

Hostilities resumed in February 2026. By that point the nuclear question was almost secondary. It was about Iran’s conventional military posture, about protests Tehran was drowning in blood, about a regime that had decided it was fighting for survival and would act accordingly.

On March 4, 2026, Iran pulled the trigger on the Hormuz blockade. Iran had threatened a Hormuz blockade so many times over so many decades that the threat had started to feel like wallpaper. Background noise. Something analysts noted, markets briefly priced, and then everyone forgot about. This time they actually did it.

How The Hormuz Blockade Sent Global Oil Into Shock

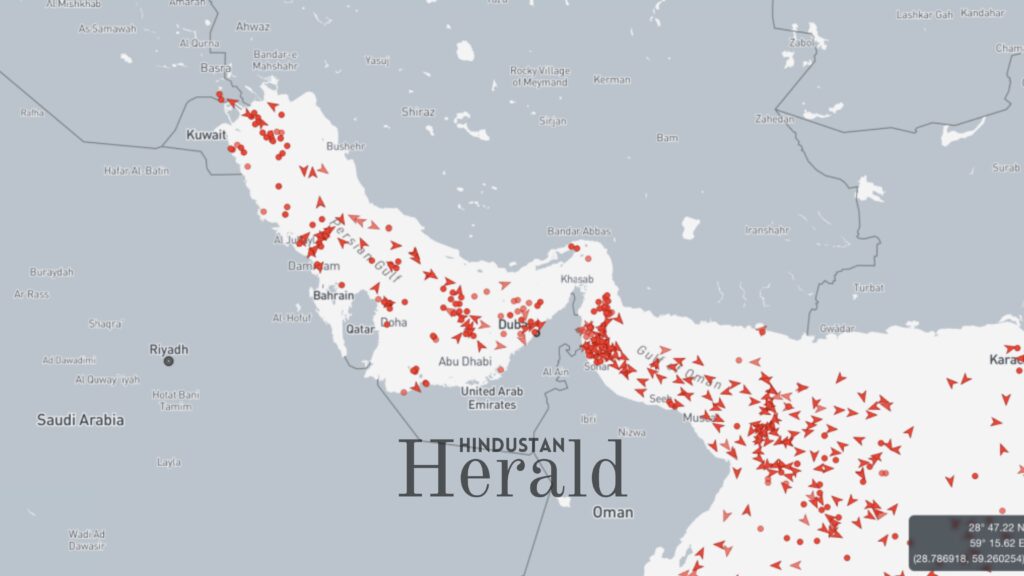

Iranian forces declared the Hormuz blockade official and began attacking ships attempting to transit. Roughly 13 million barrels of crude oil per day had passed through Hormuz in 2025, around 31% of all seaborne crude flows in the world. That flow, practically overnight, became a trickle.

IEA chief Fatih Birol called it the worst energy shock the world had ever seen. Worse than the 1970s. Worse than what Russia’s war on Ukraine did to European gas markets. That is a significant claim from a man who does not typically reach for superlatives.

Brent crude surged past $106 a barrel by late March. Before the February escalation it had been sitting around $72-75. Some desks are now running scenarios where a prolonged Hormuz blockade takes Brent toward $120, possibly higher. The number appearing in the most alarmed research notes is $150.

For a country that imports over 85% of its crude oil, those numbers are not theoretical. They are a direct hit to the national balance sheet.

How The Hormuz Blockade Caught India Dangerously Off Guard

India did not walk into this crisis from a position of energy security. It walked in already stretched.

Nearly two thirds of India’s crude oil and half the country’s LNG imports transit through Hormuz. When the Hormuz blockade began, there was no clean alternative routing available at anything close to the scale required. You cannot simply redirect 40% of your crude import flows because a chokepoint closes. The infrastructure, the shipping contracts, the refinery configurations, none of it pivots quickly.

Then the timing got worse. A US waiver that had been allowing India to buy discounted Russian crude, around 1.5 million barrels per day, expired on April 11. India had been leaning on that arrangement as a buffer while Gulf supplies tightened. With that waiver gone, India found itself facing a supply squeeze with Iranian barrels and Russian barrels both disappearing at the same time.

India has lost over 40% of its crude oil flows since the Hormuz blockade began. The state-run oil marketing companies, IOC, BPCL, and HPCL, are estimated to be bleeding up to Rs 1,000 crore per day combined, because the government is holding retail fuel prices where they are to shield consumers. That decision makes political sense. It is not a decision that can be sustained indefinitely.

5 Dangerous Ways The Hormuz Blockade Is Crushing India’s Economy

The Hormuz blockade is not hitting India through one pressure point. It is hitting through five simultaneously, each feeding into the other, each making the next harder to manage.

Way 1: India’s Crude Supply Has Collapsed

The most direct consequence of the Hormuz blockade is the one hitting hardest and fastest. India imports over 85% of its crude oil needs, making it the world’s third-largest crude importer. Nearly two thirds of those imports transited Hormuz before the blockade began. Since March 4, India has lost over 40% of its crude oil flows with no quick replacement available.

State-run refiners IOC, BPCL, and HPCL are bleeding up to Rs 1,000 crore per day as they absorb under-recoveries on petrol and diesel while the government holds retail prices artificially low. These companies had comfortable marketing margins through most of 2025. That buffer is gone. A US waiver allowing India to purchase 1.5 million barrels per day of discounted Russian crude expired on April 11, removing the one meaningful supply cushion India had left while the Hormuz blockade was already tightening everything else.

Iran did offer one carve-out. Foreign Minister Seyed Abbas Araghchi indicated that ships linked to India, China, and Russia would be permitted to transit Hormuz as a gesture toward friendly nations. India even managed to import its first Iranian oil shipment in seven years through that corridor.

Still, war-risk insurance premiums on the route have surged dramatically. Freight costs are elevated on every tanker making the run. By the time a barrel of crude arrives at an Indian refinery, the effective landed cost is significantly higher than the headline Brent price suggests. The Hormuz blockade exemption is real. The relief is not.

Way 2: Brent Crude Has Smashed Through $100

Before the Hormuz blockade took effect, Brent crude was sitting comfortably around $72-75 a barrel. The market was well supplied, OPEC+ was gradually unwinding production cuts, and India’s import bill, while significant, was manageable within the government’s fiscal calculations.

The Hormuz blockade changed that arithmetic completely. Brent surged past $106 a barrel by late March as the market absorbed the reality that 31% of global seaborne crude flows had been effectively choked. Some research desks are now running scenarios where a prolonged Hormuz blockade pushes Brent toward $120. The number appearing in the most alarmed analyst notes is $150.

Every $10 per barrel increase in Brent adds roughly $12 to $14 billion to India’s annual crude import bill. At $106 a barrel, India is paying approximately $30 more per barrel than it was before the Hormuz blockade began. That translates to an additional $35 to $40 billion on India’s import expenditure on an annualised basis, a number large enough to blow a serious hole through the current account.

The downstream effects of that price surge are working through every petroleum-linked cost in the economy. Aviation turbine fuel prices have become structurally elevated, forcing airlines into painful choices between absorbing losses or raising fares. Freight costs across road and rail logistics have climbed sharply. Naphtha and petroleum-derived inputs for paints, chemicals, and plastics manufacturers have made quarterly earnings across entire sectors look ugly.

Way 3: The Rupee Is At An All-Time Low

The Hormuz blockade has delivered a double blow to the Indian rupee that is proving difficult to defend against. The first hit came from the import side. A sharply higher crude import bill means India is spending significantly more dollars buying oil than it was six months ago. That demand for dollars to pay for crude puts direct downward pressure on the rupee through the simple mechanics of the foreign exchange market.

The second hit came from the capital account. More than $20 billion has been pulled from Indian equities by foreign institutional investors in the first four months of 2026 alone, already exceeding the full-year record of outflows set in 2025. Global funds have repriced emerging market risk upward across the board since the Hormuz blockade began, and India’s particular vulnerability to oil prices has made it a specific target for portfolio reallocation toward less exposed markets.

The combined pressure of higher dollar outflows for oil imports and lower dollar inflows from foreign investment has pushed the rupee to successive all-time lows against the dollar through April and May. A weaker rupee then makes the crude import bill even more expensive in rupee terms, creating a self-reinforcing feedback loop that is difficult to break without the underlying Hormuz blockade being resolved.

Way 4: The RBI Is Running Out Of Clean Options

In normal times, the Reserve Bank of India would respond to slowing growth by cutting interest rates, and to rising inflation by holding or raising them. The Hormuz blockade has created a situation where both problems are arriving simultaneously, leaving the RBI with no comfortable policy path available.

RBI Governor Sanjay Malhotra said this week that if the Hormuz blockade continues for several more months, the central bank may have to intervene through monetary policy, and that retail fuel price hikes may become unavoidable. That statement, carefully worded as it was, amounted to an admission that the RBI is watching a situation it cannot fully control through the tools available to it.

A fuel price hike, when it comes, will feed directly into CPI inflation, which has been running at relatively benign levels through early 2026. Tighter monetary policy in response to that inflation would slow credit growth and consumption at exactly the moment when the economy is already being squeezed by the Hormuz blockade’s impact on corporate earnings and household purchasing power.

BMI, part of Fitch Ratings, has cut India’s GDP growth forecast to 6.7% for fiscal 2026-27, down from 7.7% the previous year. That full percentage point reduction represents an enormous amount of foregone economic output and significantly complicates India’s infrastructure spending ambitions and fiscal consolidation path for the coming year.

Way 5: India’s LNG Supply Chain Is Fracturing

The crude oil story has dominated coverage of the Hormuz blockade’s impact on India, but the LNG crisis running parallel to it deserves equal attention because it is hitting a completely different set of industries with equally damaging consequences.

Qatar and the UAE together account for roughly 53% of India’s LNG imports, and both those supply routes run directly through Hormuz. When the Hormuz blockade began, that supply did not just become more expensive. It became genuinely disrupted at the source. Qatar, one of the world’s largest LNG exporters, was forced to halt production entirely after Iranian drone strikes hit its facilities at Ras Laffan Industrial City and Mesaieed Industrial City.

India’s power generation sector depends heavily on gas-fired plants to manage peak demand periods and bridge gaps in renewable supply. With LNG supply squeezed by the Hormuz blockade, those plants are running on reduced fuel availability, creating power supply pressures that are feeding into industrial production costs.

The fertiliser sector is being hit even harder. India’s domestic fertiliser production relies significantly on imported gas as a feedstock. With the Hormuz blockade cutting LNG availability, fertiliser manufacturers are facing both supply constraints and sharply higher input costs. That disruption is feeding through to agricultural input prices just as the kharif sowing season approaches, adding a food security dimension to the Hormuz blockade’s economic impact that goes well beyond energy markets.

What The Hormuz Blockade Negotiations Actually Look Like

The structure of the disagreement between Washington and Tehran has not fundamentally changed since the June 2025 breakdown. The US, pushed hard by Israel, wants Iran to give up uranium enrichment entirely. Iran insists it has the right to enrich for civilian purposes and will not sign that right away regardless of what sanctions relief is on offer.

Trump has already rejected an Iranian proposal to first end the Hormuz blockade and then deal with the nuclear question separately. His position is that the pressure stays on until Tehran moves on enrichment. Iran’s position is that the Hormuz blockade is what gets Tehran to the table, and it will not surrender that leverage without firm guarantees up front.

Iran’s Revolutionary Guard warned this week that any further strikes against Iranian territory would see the conflict extend well beyond the region. Tehran’s chief negotiator, Parliament Speaker Mohammad Baqer Qalibaf, accused Washington of preparing new military action even while the two sides were talking. Still, talks are continuing. Oman is still hosting. Both sides have said enough to keep the diplomatic channel alive, which at this stage counts as meaningful progress.

India Is Managing, Not Solving The Hormuz Blockade Problem

New Delhi has handled the Hormuz blockade crisis with the kind of studied ambiguity it has refined over decades of navigating great power competition. India has not condemned Iran’s military actions. It has not condemned the US and Israeli strikes either. It has kept diplomatic lines to Tehran open, drawn on the goodwill built through years of bilateral trade and the Chabahar port project, and quietly leveraged that relationship into the partial Hormuz blockade exemption that has kept some supply flowing.

That positioning has worked, to a point. But India is also discovering that Washington’s policy choices are creating real costs for New Delhi even as the two countries draw strategically closer. The expiry of the Russian crude waiver is the most pointed example. India was expected to align with Western sanctions policy. It did. And then it lost a critical supply source at exactly the wrong moment, with the Hormuz blockade already squeezing everything else.

Petroleum Minister Hardeep Singh Puri’s team is working every available alternative. Sourcing crude from West Africa and the Americas costs more in freight, takes longer in transit, and does not match the refinery configurations Indian plants have spent years optimising for Gulf crude grades. But working every option when the Hormuz blockade has cut 40% of your crude flows is a fundamentally different problem from having those flows intact in the first place.

Where The Hormuz Blockade Crisis Eventually Lands

For investors tracking India macro, the forward scenario is not complicated to map, even if the timing remains deeply uncertain. A deal that credibly ends the Hormuz blockade brings Brent back toward $70-75, restores OMC marketing margins, stops the rupee slide, takes inflationary pressure off the RBI, and begins unwinding the FII outflow story weighing on equities since March. The market recovery in that scenario would be swift and broad, touching everything from refinery stocks to airlines to two-wheeler manufacturers watching rural demand soften under fuel price pressure.

No deal, or another round of escalation, means the Hormuz blockade drags on, the government eventually has no choice but to raise retail fuel prices, the RBI faces a monetary policy choice with no good options, and India’s growth story takes a hit that will take years to fully recover from.

The answer is sitting somewhere in a negotiating room in Muscat or Geneva, between two governments that deeply distrust each other. One is threatening military action. The other has already imposed the Hormuz blockade that has become the most consequential energy disruption the world has seen in decades. Trump says the talks are in their final stages. India hopes, for reasons that have everything to do with economic survival and nothing to do with geopolitical alignment, that he is right this time.

Stay ahead with Hindustan Herald — bringing you trusted news, sharp analysis, and stories that matter across Politics, Business, Technology, Sports, Entertainment, Lifestyle, and more.

Connect with us on Facebook, Instagram, X (Twitter), LinkedIn, YouTube, and join our Telegram community @hindustanherald for real-time updates.

Tracking world politics, global markets, trade movements, policy decisions, and the changing balance of economic power.

- Shelesh Joshi

- Shelesh Joshi

- Shelesh Joshi

- Shelesh Joshi

Former financial consultant turned journalist, reporting on markets, industry trends, and economic policy.

- Kavita Iyer

- Kavita Iyer

- Kavita Iyer

- Kavita Iyer