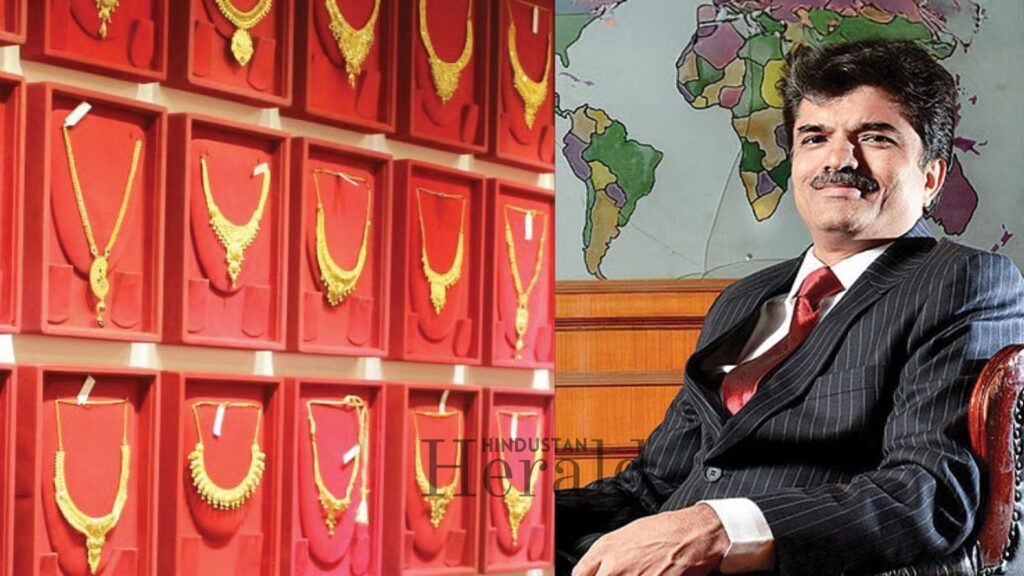

Mumbai, June 5: India’s Biggest Revenue Fraud Allegation: SEBI Drops a 109 Page Bombshell on Rajesh Exports and Promoter Rajesh Mehta The Rajesh Exports SEBI Order has shaken the country’s corporate governance establishment in a way few regulatory actions have in recent memory.he gold that Rajesh Exports claimed to be refining and trading across continents may have generated little more than numbers on a spreadsheet. That, in essence, is what India’s most powerful markets regulator has alleged in a sweeping interim order that rattled institutional investors and sent one of the country’s highest revenue companies crashing into a lower circuit in a matter of hours.

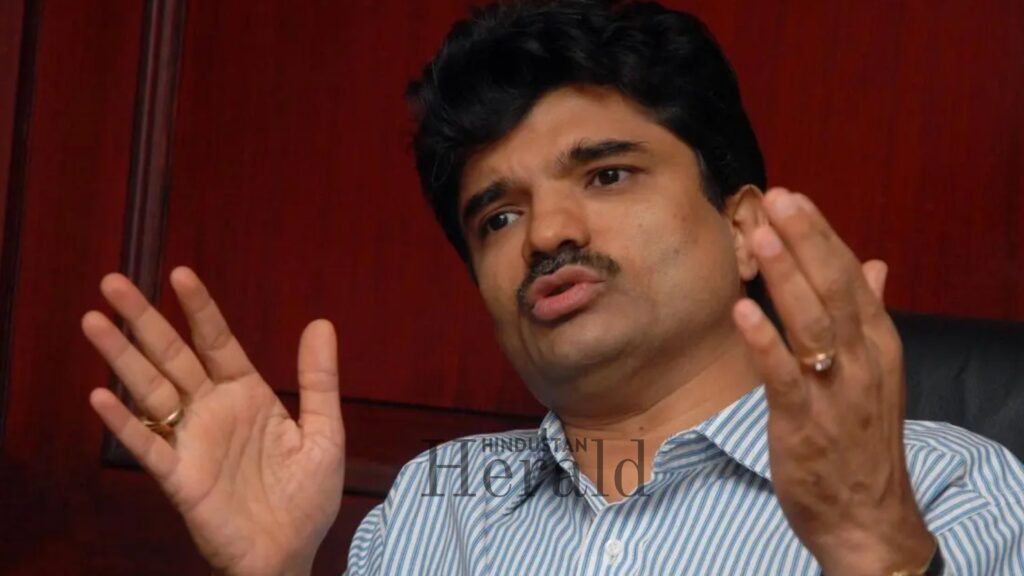

On June 3, 2026, the Securities and Exchange Board of India (SEBI) issued a 109 page interim ex parte order against Rajesh Exports Limited, a Bengaluru based gold jewellery and refining firm, and its Chairman and Managing Director Rajesh Mehta. The order was authored by SEBI Whole Time Member Kamlesh Chandra Varshney. As confirmed by Moneylife, the regulator levelled allegations of widespread financial misrepresentation of approximately Rs 15.15 lakh crore, non disclosure of material information, questionable accounting practices, and misuse of corporate funds across five financial years. Both the company and its promoter chairman have been restrained from accessing the securities market pending further directions.

Quick Summary

- According to the SEBI interim order, as confirmed by both Business Standard and BusinessToday, Rajesh Exports misrepresented consolidated revenues aggregating approximately Rs 15.15 lakh crore between FY2020-21 and FY2024-25, accounting for nearly 99.8 per cent of the company’s total reported consolidated revenue from subsidiaries during the period.

- As reported by Outlook Business, SEBI estimated shareholder wealth erosion linked to the alleged misconduct at up to Rs 12,726 crore. Life Insurance Corporation of India (LIC) holds approximately 10.8% of Rajesh Exports, a stake ultimately backed by the premiums of ordinary Indian policyholders.

- According to Outlook Business, shares of Rajesh Exports fell 5% on June 4, hitting the lower circuit at Rs 103.92, extending a decline that has seen the stock lose more than 80% of its value over the past three years.

- As per the SEBI interim order, cited by BusinessToday, Rajesh Exports reported sales of Rs 11,487 crore and purchases of Rs 11,488 crore with Affluence Shares and Stocks Pvt. Ltd, but Affluence denied that any such transactions had ever taken place.

- As reported by NewsX, SEBI accused Rajesh Exports of channelling approximately Rs 338.90 crore of company funds into accounts held by promoter Rajesh Mehta without board authorisation or proper disclosure.

- According to India Infoline, Canara Bank has reportedly classified its exposure to the company as a stressed asset, with dues estimated at around Rs 509 crore, and has initiated steps to auction the exposure.

How a Single Shareholder Complaint Opened the Rajesh Exports SEBI Order Investigation

The road to the Rajesh Exports SEBI Order began not in a regulatory boardroom but with a single shareholder who noticed something that did not feel right about Rajesh Exports’ books.

As reported by Outlook Business, the matter came to light through a shareholder complaint filed with SEBI in March 2024. The complainant alleged potential financial misrepresentation, flagging a large sum of trade receivables that had remained outstanding for over two years. In accounting terms, trade receivables are amounts customers owe a company for goods already sold and delivered. When those amounts sit unpaid for years, they raise a fundamental question: were those underlying sales transactions real in the first place?

According to Business Standard, SEBI initiated a formal investigation in October 2024 and subsequently engaged forensic auditor BDO India Services to examine the company’s financial disclosures. As per the same publication, the investigation moved beyond unpaid receivables when SEBI’s interim order noted that out of transaction samples worth more than Rs 7,000 crore, complete supporting documentation was provided for only a small fraction of the total value examined. That finding shifted the probe from a narrow receivables query into a full scale examination of whether the company’s broader financial reporting could be independently verified at all.

According to Outlook Business, investigators faced significant obstacles at every stage of the Rajesh Exports SEBI Order proceedings. Rajesh Exports did not provide complete customer records, vendor details, or financial statements of key subsidiaries despite repeated summons from the regulator. The company’s statutory auditors came under scrutiny as well. Having committed during depositions before SEBI to submit their audit working papers, they subsequently failed to do so.

That refusal to produce working papers, after having committed to deliver them, factored significantly into the regulator’s decision to pass an interim ex parte order, an approach SEBI reserves for situations where it believes assets may be dissipated or evidence concealed if the subject is given prior notice.

The Valcambi Problem: Trillions on Paper, Hundreds of Crores in Reality

At the beating heart of this case sits Valcambi SA, a Switzerland based precious metals refinery that Rajesh Exports had positioned as the crown jewel of its global operations and the principal driver of its enormous consolidated revenue numbers.

As laid out in detail by Business Standard, the corporate structure that SEBI examined placed Rajesh Exports Limited at the top. Below it sat REL Singapore, described by the company itself as a holding company without significant day to day operations. REL Singapore owned Global Gold Refineries AG (GGR), a Switzerland based entity also characterised as a holding company. GGR in turn owned Valcambi SA, the Swiss refinery that the company repeatedly described as the group’s principal operating entity. According to SEBI, these overseas subsidiaries were not peripheral businesses. They were effectively the entire group, generating between 97% and 99% of Rajesh Exports’ consolidated revenues in every year from FY21 through FY25.

That concentration of revenue in overseas entities would warrant careful scrutiny under any circumstances. What SEBI found when it tried to verify those revenues against Valcambi’s own audited records made the picture significantly more alarming. As confirmed by both Business Standard and BusinessToday, drawing from the SEBI interim order, Valcambi SA reported annual standalone revenues ranging from roughly Rs 427 crore to Rs 743 crore during the corresponding years. By contrast, group entity GGR and Rajesh Exports were reporting consolidated revenues running into several trillion rupees.

Outlook Business reported the single year comparison in the starkest possible terms: in CY2023, Valcambi’s standalone audited revenue stood at just Rs 542.68 crore, a figure confirmed by both Outlook Business and IndMoney directly from the SEBI order. In that same period, group entity GGR reported consolidated revenue of approximately Rs 2.92 to Rs 2.93 lakh crore, while Rajesh Exports reported approximately Rs 2.80 to Rs 2.81 lakh crore at the consolidated level.

The minor one decimal variance in the GGR and Rajesh Exports consolidated figures exists across publications due to rounding differences Outlook Business cites Rs 2.93 lakh crore for GGR and Rs 2.81 lakh crore for Rajesh Exports, while IndMoney cites Rs 2.92 lakh crore and Rs 2.80 lakh crore respectively for the same entities in the same period, both drawing from the SEBI order. The rounding difference does not affect the substance of the finding. What matters is that Valcambi’s verified standalone revenue of Rs 542.68 crore sat alongside group level consolidated revenues of several lakh crore, a gap of several hundred times the auditable number at the entity that was supposed to be generating it all.

Rajesh Exports had an explanation ready, and it is worth setting out fairly. The company told SEBI, as reported by Business Standard, that Valcambi’s standalone accounts reflected only processing charges and value addition income, while GGR recognised the full gross value of gold transactions.

This is a distinction that does exist legitimately in the commodities world. A refinery that processes gold owned by a client may book only its processing fee, while a trading entity that takes legal ownership of gold and then sells it books the entire transaction value as revenue. The question SEBI asked, and could not get answered to its satisfaction, was whether the company could produce any documentation at all to support that accounting treatment.

As per Business Standard, SEBI found that the company failed to provide sufficient documentation, accounting opinions, ownership records, reconciliation statements, or transaction level evidence to substantiate this treatment, despite repeated requests. SEBI Whole Time Member Kamlesh Chandra Varshney raised a precise and pointed question directly in the order text, as quoted by Outlook Business: “It is not clear as to how the consolidating entity changes fundamental of accounting by including the market value of goods belonging to third party as its revenue, when the operating entity itself accounts for only value addition, as it does not claim to take ownership of goods belonging to someone else.”

That question is now one that every auditor, analyst, and investor tracking Indian gold and commodities companies will need to sit with carefully.

The Affluence Shares Thread: Transactions That Never Happened

Beyond the Valcambi revenue structure, a second and separately troubling layer runs through the SEBI order. According to BusinessToday, which cited the SEBI interim order directly, Rajesh Exports had reported sales of Rs 11,487 crore and purchases of Rs 11,488 crore with an entity called Affluence Shares and Stocks Private Limited. When investigators went to Affluence to verify these transactions, Affluence denied that any such transactions had taken place.

As reported by BusinessToday, SEBI alleged that these were non genuine accounting entries, linked to promoter Rajesh Mehta’s personal gold derivative trades, and were recorded in Rajesh Exports’ books as company transactions. As noted by IndMoney in its analysis of the order, the near equal amounts of reported sales and purchases from the same counterparty meant there was almost no real value addition from the arrangement.

Such entries can be used to make a company look much larger in revenue terms without generating any meaningful underlying business activity. For investors who track turnover as a measure of operational scale, such entries, if proven to be fictitious, represent a direct misrepresentation of the company’s true commercial footprint.

Fund Routing Through Personal Accounts and a Promoter Linked EV Firm

SEBI’s order did not stop at revenue misrepresentation. It went further, into the question of where the company’s actual cash flows were going and who was directing them.

As reported by BusinessToday, drawing directly from the SEBI interim order, the regulator alleged that Rajesh Exports routed Rs 338.90 crore of company funds specifically into accounts linked to promoter Rajesh Mehta, including for his personal derivative trades, without obtaining board or audit committee approvals and without making proper related party disclosures.

That figure, however, is not the complete picture of what SEBI found. As separately reported by BusinessToday in a second article citing the same SEBI order, the regulator alleged that in total, Rs 926 crore was routed through such transactions linked to Mehta without the required board approvals or disclosures. The Rs 338.90 crore represents the amount traced specifically to accounts directly held by Mehta, while the broader Rs 926 crore figure covers the full scope of allegedly unauthorised fund routing across all linked accounts and entities flagged in the order.

Both figures originate from the SEBI interim order dated June 3, 2026, and are reported by BusinessToday. As reported by IndMoney, SEBI also alleged that company funds were routed through the personal accounts of Siddharth Mehta and through promoter linked entity Elest, and that several of these transactions were never placed before the board or audit committee for approval and were not disclosed as related party transactions to shareholders.

When a listed company routes hundreds of crores through personal accounts and promoter linked entities without board sanction, it undermines the foundation of minority shareholder protection that India’s listing obligations framework is designed to enforce.

The Elest thread carries its own distinct and serious texture. As reported by Outlook Business, SEBI flagged a cross holding arrangement involving ACC Energy Storage, Rajesh Exports’ own energy storage subsidiary. On January 1, 2025, Rajesh Exports acquired an additional 2.55 crore shares of ACC Energy at Rs 60 per share, while Elest simultaneously subscribed to 2.45 crore shares at the exact same valuation.

Following these transactions, Rajesh Exports’ stake in ACC Energy fell from 100% to approximately 51.05%, while Elest’s shareholding rose to about 48.95%. SEBI’s preliminary analysis of bank statements, as reported by the same publication, showed that Elest transferred Rs 147 crore to ACC Energy, of which Rs 112 crore was transferred back to Elest on the very same date.

What makes this exchange particularly disturbing is the testimony of the company’s own senior management. According to Outlook Business, SEBI noted in its order that Rajesh Exports’ Managing Director Suresh Gowda and CFO Vijendra Rao, in their depositions before the regulator, stated that they were entirely unaware of Elest’s Rs 147 crore investment in ACC Energy, and were equally unaware of a subsequent Rs 262 crore investment by ACC Energy back into Elest.

Two of the most senior executives of a listed company professing complete ignorance of transactions worth hundreds of crores involving their own subsidiary is not a procedural lapse. It signals a systemic breakdown of internal governance and oversight.

The African Gold Mine That Cannot Be Found

In a case already crowded with serious allegations, one claim stands apart for the near total absence of any supporting documentation. As reported by Outlook Business, SEBI noted in its order that Rajesh Exports’ other non current investments on a consolidated basis rose from Rs 879.60 crore in FY21 to Rs 1,035.27 crore in FY23, before jumping sharply to Rs 10,547.72 crore in FY25. That sharp upward move warranted explanation.

As reported by The Federal, when the National Stock Exchange (NSE) asked the company to explain the Rs 1,035.27 crore figure reported as of March 31, 2023, Rajesh Exports responded in July 2024 by saying the amount pertained to investments in gold mines in Africa. As per the same report, SEBI’s interim order recorded that the company was unable to furnish any documentation supporting the existence or valuation of those investments.

Asserting in an exchange filing that over a thousand crores are parked in African gold mines, without a single contract, valuation certificate, mine record, or ownership document to support the claim, is precisely the kind of undocumented assertion that the SEBI order described as egregious.

The Market Verdict: Three Years of Erosion, Then a Lower Circuit

The stock market delivered its judgment with characteristic speed. As reported by Outlook Business, shares of Rajesh Exports fell 5% on June 4, hitting the lower circuit at Rs 103.92, a day after the SEBI order was issued. The stock had already been under sustained pressure before the regulatory action. According to Univest, the 52 week high stood at Rs 237.88 while the 52 week low was Rs 80.38, with the stock declining approximately 46.85% in the year prior to the order.

Stepping back further, as reported by both Outlook Business and India Infoline, the stock has lost more than 80% of its value over the past three years, reflecting a prolonged erosion of investor confidence driven by debt concerns, operational difficulties, and governance questions that predated the SEBI order.

The fallout did not stay contained to Rajesh Exports itself. As reported by NewsX and Connected to India, shares of Life Insurance Corporation of India (LIC), which holds a 10.80% stake in the company, declined by more than 1% on the day the order became public. LIC’s position in Rajesh Exports is not a speculative trading stake.

It is backed by the insurance premiums and long term savings of millions of ordinary Indian households who have no direct knowledge of Rajesh Exports, Valcambi, or the regulatory proceedings underway. The wealth erosion estimated by SEBI at Rs 12,725.53 crore, a figure cited by both BusinessToday and Outlook Business directly from the SEBI order, carries human consequences that reach well beyond capital markets.

As an additional pressure point, India Infoline reported that Canara Bank has reportedly classified its exposure to Rajesh Exports as a stressed asset following repayment defaults, with outstanding dues estimated at around Rs 509 crore, and the bank has initiated steps to auction the exposure. A simultaneous regulatory bar, an 80% stock decline over three years, and a lender moving to auction its stressed loan is a combination that leaves very limited room for operational recovery.

The Auditor Question That the Entire Industry Must Answer

Every major governance failure in India’s listed company space eventually arrives at the same uncomfortable question: where were the auditors?

The SEBI interim order cited prima facie misconduct and dereliction of duties by the company’s statutory auditors, as confirmed by Moneylife. According to NewsX, the matter has been referred to the National Financial Reporting Authority (NFRA) for independent examination of the auditors involved. That referral to NFRA, the body that regulates and disciplines the audit profession in India, signals that the consequences of this case will not be confined to Rajesh Exports alone.

The firms and individuals who signed off on five consecutive years of financial statements in which, according to the regulator, nearly the entire revenue base could not be independently verified, face a separate scrutiny track that will run in parallel to the core SEBI proceedings.

As noted by Outlook Business, the statutory auditors had committed in depositions to produce their audit working papers and subsequently failed to do so. If those working papers showed robust and documented verification of Valcambi’s revenues and the overseas subsidiary structures, the company would have produced them at the first opportunity. Their absence from the record is, in the regulator’s assessment, itself a significant finding.

This case lands at a moment when India’s audit quality debate was already intensifying. SEBI’s order on Rajesh Exports will provide regulators, standard setters, and institutional investors with renewed urgency to examine whether the current disclosure and verification framework is structurally adequate for companies whose entire revenue base flows through overseas subsidiaries with limited public transparency.

Rajesh Exports Fights Back: “Nothing in It Is True”

The company and its promoter have not accepted SEBI’s characterisation without challenge, and their position deserves fair and complete reporting.

Rajesh Mehta was categorical in his initial public response. As reported by Outlook Business, which cited Moneycontrol as the original platform, Mehta stated on June 4: “It is an interim order and nothing in it is true. We are in the process of studying it and will prepare a response.”

In a formal filing to stock exchanges on June 4, the company said, as reported by The Federal and Moneylife: “The revenues declared by the company are correct, and there is no over stating of revenues. There seems to be some type of communication gap and confusion between SEBI and the company.”

The company added that the order is interim in nature, that SEBI has not reached any adverse final conclusion on any aspect, and that it is actively submitting all required and relevant documents to the regulator. According to Moneylife, the company expressed confidence that SEBI would arrive at a correct understanding of the situation once all documentation was reviewed.

These positions must be afforded full weight. The order is interim. These are prima facie findings, not final adjudicated conclusions. Rajesh Exports and Rajesh Mehta retain the complete right to present their defence, produce supporting documents, and contest every allegation before a final order is issued.

The accounting explanation around gross transaction recognition at the consolidation level is not inherently implausible. The question is whether documentation exists to support it and whether it will be produced within the 30 day window SEBI has set. As directed by SEBI and confirmed by Outlook Business, the regulator has also ordered the appointment of a new forensic auditor to complete the examination of the company’s books.

What Comes Next and Why This Case Will Define Indian Corporate Governance

The proceedings will now move toward a formal hearing, where both sides will place evidence and arguments before SEBI. Given the cross border complexity involved, including Swiss corporate structures through GGR and Valcambi, unsubstantiated African investment claims, Singapore holding companies with no substantive operations, and EV related fund flows within India through Elest and ACC Energy, this is expected to be a prolonged and technically demanding regulatory process.

For now, the broader market and the broader investing community are watching closely. This case touches almost every pillar of investor protection simultaneously: revenue transparency, subsidiary disclosure standards, related party transaction governance, auditor accountability, and the adequacy of forensic verification for complex multinational holding structures.

For the retail investors and LIC policyholders whose savings are embedded in this company’s declining valuation, the stakes are entirely real. And for India’s regulatory architecture, this case may well become the benchmark by which the adequacy of consolidated financial disclosure standards is measured for years to come.

As SEBI Whole Time Member Kamlesh Chandra Varshney observed in his 109 page order, citing the Moneylife report, the aberrations noted in this matter, where approximately 97% to 99% of the revenues of the company are alleged to have been inflated, are “egregious and unheard of.” That assessment, from the pen of a senior SEBI official, tells you everything about the gravity of what is being alleged and what India’s capital markets now have to work through.

Stay ahead with Hindustan Herald — bringing you trusted news, sharp analysis, and stories that matter across Politics, Business, Technology, Sports, Entertainment, Lifestyle, and more.

Connect with us on Facebook, Instagram, X (Twitter), LinkedIn, YouTube, and join our Telegram community @hindustanherald for real-time updates.

Tracking world politics, global markets, trade movements, policy decisions, and the changing balance of economic power.

- Shelesh Joshi

- Shelesh Joshi

- Shelesh Joshi

- Shelesh Joshi

Former financial consultant turned journalist, reporting on markets, industry trends, and economic policy.

- Kavita Iyer

- Kavita Iyer

- Kavita Iyer

- Kavita Iyer